%201.svg)

What is Job Order Costing?

Job order costing (or job costing) is a method for calculating the costs of manufacturing a single product.

It’s a technique primarily used by manufacturers that produce bespoke or custom projects, such as construction, which involves partial or full completion of a building.

Because there is significant variation in the items manufactured, a manufacturer using the job order costing system requires a separate job cost sheet for each item or final output. This document will detail each item’s direct materials, direct labor, and manufacturing overhead, enabling a business to determine profitability, accurately price bids, and analyze efficiency for distinct products and jobs.

The job cost sheet will also serve as the subsidiary ledger and documentation for the manufacturer’s costs of work-in-process inventory, finished goods inventory, and cost of goods sold.

What Are the Three Elements of Job Costing?

If you’re a business that produces non-standardized products, you’ll need to look into the following three cost centers for making your job order costing calculations:

- Direct materials

- Direct labor

- Manufacturing overhead

Understanding the costs of these three areas will help you track profitability and better manage your expenses. But what are they?

1. Direct Materials

These are the raw materials, components, or subassemblies required to produce a finished product or deliver a service. However, you should also factor in the consumables you need for the job, such as glue, nuts, and bolts. It might not seem important, but even the smallest oversights in material usage can skew your profitability calculations, so ensure you’re tracking these as well.

Here is the formula for calculating direct material costs:

Direct material cost = [(Raw material cost + Indirect tax) – Discounts] + Freight-in + Storage + Packing

2. Direct Labor

This one is relatively straightforward, but calculating your direct labor costs requires considering the people involved in producing the finished product. So, your employees' wages, salaries, and benefits, as well as their supervisors, and any contractors you may need to bring in to complete an order.

Here is the formula for calculating direct labor costs:

Direct Labor Cost = Hours Worked × Hourly Rate

3. Manufacturing Overhead

Finally, we look at the costs required to complete a project or product. This includes your rent, utilities, machinery depreciation, and indirect labor, from the people on your HR team to the janitors keeping the shop floor clean. As this is the trickiest thing to calculate (close to impossible even), most businesses rely on a predetermined rate, often based on labor hours or machine hours

Here is the formula for calculating manufacturing overhead:

Manufacturing Overhead = Indirect labor + Indirect materials + Factory utilities + Depreciation + Insurance + Other indirect factory costs

Job Order Costing vs. Process Costing

Another term you have likely stumbled across is process costing.

How this differs from job order costing is that process costing tracks the average cost over large batches of products, such as finished goods that come off an assembly line. Here, costs are assigned at the department/process level to calculate an average across units for a production run. If you want to know which one is the best for your business, you can think of it like this:

- Job order costing: For a business that provides a custom service or manufactures unique, client-specific products.

- Process costing: For a business that produces large quantities of the same standardized product, such as food production.

However, it doesn’t have to be one or the other. If you’re a business that provides standardized and customized products, like assembling PCs, you can use both methods for specific productions runs.

5 Reasons Why Job Order Costing is Important

Ultimately, the major goal of almost all businesses is making a profit, and job order costing is going to ensure that you’re properly pricing your jobs, performing profitability analysis, improving resource allocation, and making data-driven decisions for all your future projects.

Looking into these costs not only helps improve your financial health, but it is also essential to start using job order costing in your business for a range of other benefits you might not have considered at first glance.

1. Determining Profitability

Job order costing helps you estimate how much material, labor, and overhead will be used for a specific job.

If done efficiently, it will allow you to create and send quotes to clients, ensuring you don’t incur costs that take you into the red, while remaining competitive, and giving your client a fair price. Another way job order costing helps improve profitability is by helping you identify cost variances, analyze their causes, and implement corrective actions.

Now, instead of blindly agreeing to take on a project, you’ll understand:

- The budget needed to complete a job

- How much money is required to be profitable

- Which clients are costing you profit

- Whether you have enough resources to complete a job

2. Making Better Business Decisions

Over time, as you use job order costing, you will build a database that will help you better price jobs every time an order comes in.

But, this only works if you store this information and use it to evaluate your efficiency. What this means in practice is analyzing historical jobs to eliminate anything that unnecessarily adds cost, such as changes to processes, resources, or even staffing (which we will explore further later). Again, this only works if the information is saved, which is why many manufacturers turn to manufacturing ERP software to automate documentation and analysis.

3. Monitoring Machine Usage

Using job order costing, you’ll see how much you’re using machines and tools as the costs are distributed across all your different jobs.

Since you’ll need to think about what machinery a job requires and how much you’ll end up using it, you’ll actually have a way to monitor its usage overall. This means you can start managing the maintenance and replacement cycles for your machines and tools.

4. KPI and Client Management

As you start to investigate your costs and build your database, you’ll be able to use this information to see which employees, departments, and teams are the most and least productive.

You’ll be able to do this because, if costs are high, you will need to identify inefficiencies in labor or material use that are driving them. The same goes for clients. As you build a more accurate picture of what it takes to complete a job, you can determine which clients need to be re-priced or let go.

5. Identifying Low-Hanging Fruits

For some businesses, such as start-ups or those facing constraints such as market volatility or a shortage of skilled labor, job costing helps identify opportunities with the highest potential for gross profit.

So, what started as an exercise to determine how much it costs to make something has become a data hub that not only helps make better decisions (as mentioned before) but can also be repurposed to change a business's direction completely.

Calculating Job Order Costing in 6 Steps

To be effective, job costing must go beyond tracking expenses and focus on turning project data into useful financial insights. From the beginning of the job through final reporting and analysis, each of the six steps below builds on the previous ones to paint a detailed picture of a project’s costs and profitability.

Now that we understand the ins and outs of job order costing, we can get into the nitty-gritty.

Here is a step-by-step guide to performing costing from the moment a client requests a new project through final reporting and analysis.

Step 1: Identifying and Defining the Job

When estimating the costs, you’ll need to create a system for projecting, tracking, and analyzing how much the job will cost.

This will include things like:

- Defining the scope of the project

- Mapping out the deliverables

- Setting deadlines

Once you have that, you can create a unique code to identify the job so expenses can be tied back to that specific project. An example of the code could be [ClientName-OrderNumber] (BOB-012). Next, use the fields to track all associated costs, such as labor hours, material purchases, subcontractor invoices, and anything else you need to complete this project.

This might sound tedious. As explained earlier in the article, because you’re making unique products for each order, it is essential to treat each order as a project.

Step 2: Listing Direct Materials

We’re including this step because it supports the next step, but it doesn’t hurt to include the direct materials you’ll need to consume while fulfilling this order.

This will help you determine whether you have enough material on hand to fulfill the order. You might scoff and think this is obvious. The only reason we highlight it is that if you don’t have enough, you’ll need to order more, and the cost of ordering those materials will change how much it costs you to complete the project.

Step 3: Estimating the Cost of the Job

At this stage, you know what resources you’ll need to finish the job on time — now comes the calculations.

To estimate the job cost, you will need to calculate:

- Labor

- Material

- Overhead

This is easier if you have past projects you can draw on to estimate these costs, while also monitoring current market rates and defining the project's specific requirements. So, what exactly are you looking for when estimating these costs? Check for:

- Direct Materials: Looking into the sum of all the raw materials being directly used in the job

- Direct Labor: Take your worker(s) or contractors' pay rate and multiply that by the hours they will spend working on the job (including taxes/benefits)

- Manufacturing Overhead: This includes rent and utilities divided by the hours it will take to complete the project

Once you have all this information, you can go ahead and calculate the job order cost using the following formula:

Job Order Costing = Direct Materials + Direct Labor + Manufacturing Overhead

We’ll include an example later in the article.

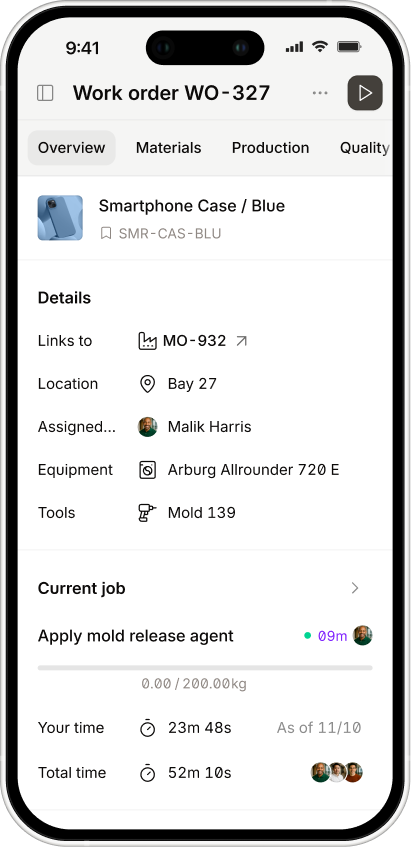

Step 4: Tracking and Recording Costs

So, you have your job order cost calculations — now it’s time to verify whether they're correct.

First, you should save your calculation as a planned cost, preferably using a job cost sheet or job cost accounting software. Once that is done, and production begins, you should be tracking all the actual costs of the job, including things like:

- Recording receipts

- Timesheets

- Invoices

- Purchase orders

This will ensure that you’re not going over budget and that you can readjust if needed during the project, which brings us nicely to the next step.

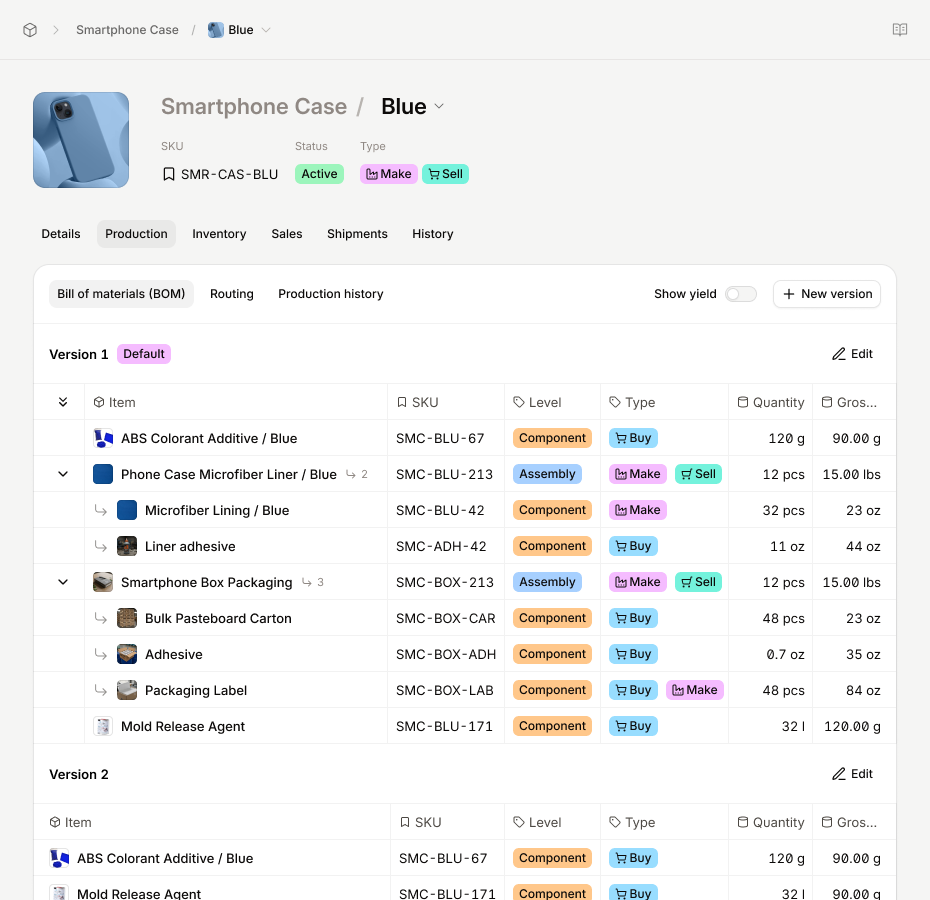

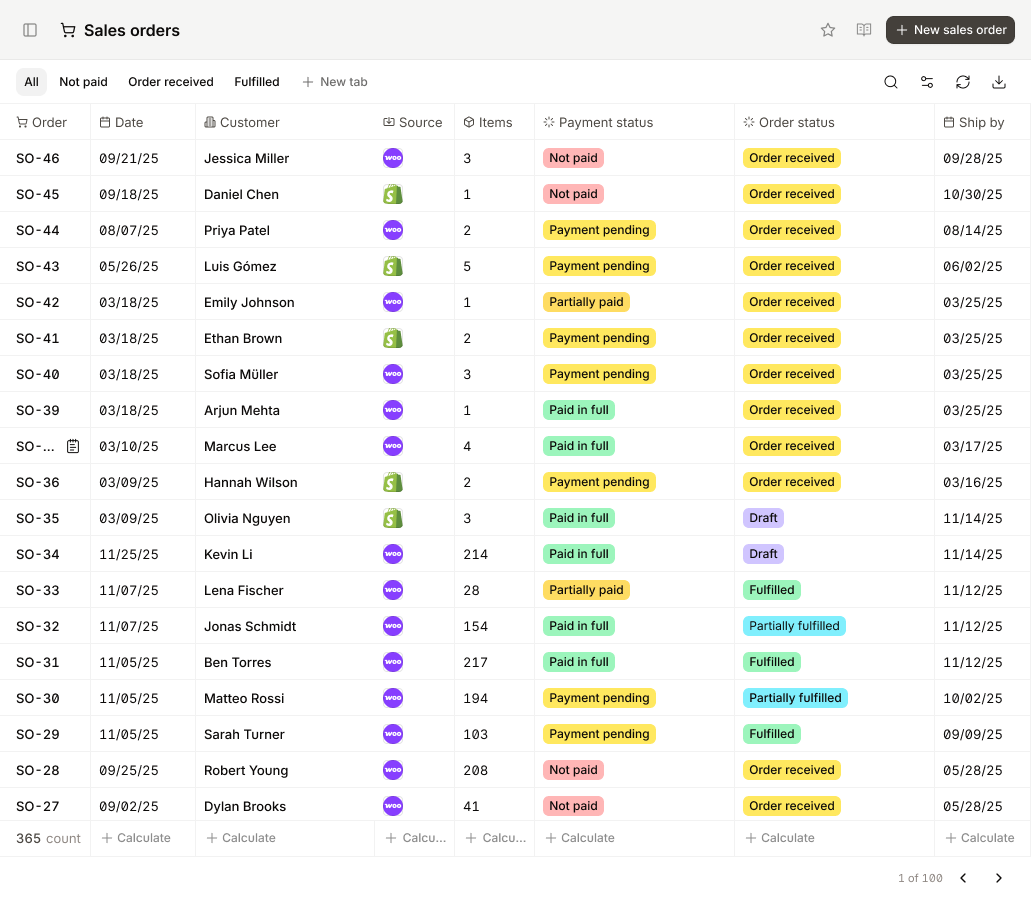

What is a Job Order Cost Sheet?

A job order cost sheet is a report that lists all costs for a single job.

Businesses use it to see how much a job really costs and whether it made a profit. The accounting team prepares the job cost sheet and shares it with managers to verify that the job was priced correctly. It is usually finished after the job is done, but it can also be updated while the work is still in progress.

Step 5: Analyzing Costs

If you under- or overestimated the project cost, comparing planned and actual costs will help you identify variances, calculate profit margins, and reveal inefficiencies.

Perpetual analysis will help you identify issues and take corrective actions before costs spiral out of control.

Step 6: Creating Reports

Each time you finish a job, it should include total costs, profitability, and performance.

You can use these reports internally to refine your pricing strategies and create a reference library that will help you in the future to better scope and price projects.

Below is an example to help you better understand how to perform job order costing.

Job Order Costing Example in Action

Let us introduce you to John and Jane, a married millennial couple who run a small business building custom PCs out of a small office in a hip, gentrified part of town.

John assembles the PCs, and Jane manages all back-office responsibilities. They average three orders a month. Luckily for them, Jane told John that a client had contacted them requesting a gaming PC, and they would need to send a quote.

Here is all the information they will need to consider for making their calculations:

- Component (CPU, GPU, motherboard, RAM, etc.) — $2,000

- Inbound freight of the components — $50

- Shipping to the client — $25

- The time to build — 1.5 hours

- Wage for John and Jane — $75/hour

- Rent and utilities — $500/month

Starting with the direct material costs, which will contain components, freight, and shipping (shipping can be tracked separately, but since we have the cost here, we’ll include it for a more accurate estimate):

Direct Materials: $2000 + $50 + $25 = $2,075

Next, we’ll calculate direct labor. In this case, John is assembling the PC, so we need to consider only his costs and the build time at this stage:

Direct Labor: 1.5 × $75 = $112.50

Finally, we can begin examining manufacturing overhead. But let’s spice it up. John only works when something needs to be assembled. Jane, on the other hand, is the brains of the operation, working 20 hours a month.

First we need to figure out how much she makes in a month:

Jane’s Pay: 20 x $75 = $1,500

We can now include rent and utilities, bringing the monthly manufacturing overhead to $2,000. This helps us calculate our predetermined rate, which is the working hours divided by the monthly overhead:

Predetermined Rate: $2,000 ÷ 20 hours = $100

We’re nearly at the finish line! With the rate determined, we can finally calculate the manufacturing overhead costs for this job, which will be:

Manufacturing Overhead (for this job): 1.5 x $100 = $150

And the last step, now that we have all the info we need, is calculating the job order cost:

Job Order Cost: $2075 + $112.50 + $150 = $2,337.50

Once you have this number, remember to include a markup in the quote you send to the client. A rule of thumb is to have a markup of 40% (in this case, the client will pay $3,272.50).

And there you have it, all the essential information you need to start estimating the job order cost for your projects. However, as already mentioned, this process (without the use of software) can be tedious as you need to manually check and update your figures as things change, and it is supposed to be used only as an estimate. Your job order cost sheet will contain info on your actual costs.

For these reasons, many turn to tools like Digit to help them manage their manufacturing costs.

How You Can Use Digit for Job Order Costing

Keeping track of job costs manually can work at a small scale, but as order volume grows, it quickly becomes time-consuming and error-prone.

This is where tools like Digit help manufacturers manage their costs more effectively. Digit uses actual costing, which means every item produced tracks its real cost based on what actually happens during production. As materials are picked, labor time is logged, or outputs are created, Digit automatically updates the cost, giving you a clear, up-to-date view of material, labor, and overhead costs tied to each manufacturing order.

To avoid confusion during production, Digit also distinguishes between pending costs and final costs.

While a job or subassembly is still in progress, its cost is marked as pending. Once all related work orders are completed, the price is finalized and locked in. This makes it easier to understand which numbers are estimates and which are ready for accounting and reporting.

By tracking costs in real time and clearly labeling what’s still in progress, Digit helps manufacturers maintain an accurate job order cost sheet, produce reliable COGS reports, and make better pricing and profitability decisions.

Book a demo today and see how you can automate your costing process.

.jpg)

.jpg)